-

Resources

Adopt the Best Funding Model for Your Plan

Are you applying the right funding model to each benefits category? To find out, we’ve broken down some of the questions you should ask yourself first, to make an informed decision.

Pooled vs Experience Rated Benefits

These benefits can be broken down into two categories, and we will explore the differences between them both below.

Pooled benefits include life insurance, accidental death and dismemberment (AD&D), dependent life, long-term disability, and out of country travel. Pooled benefits are a small part of your monthly group insurance premiums. They are usually unpredictable in nature, typically for catastrophic events, such as disability or even death.

Experience rated benefits are healthcare, prescription drugs, dental, vision care, and short-term disability. These benefits make up the majority of your monthly group insurance premiums. They are much more predictable in nature and are best for repetitive, day-to-day events, such as check-ups, drug renewals, or glasses.

The rates for each benefit type are calculated differently. Pooled benefits rates are based on a combination of the insurer’s total claims losses in the marketplace and the employee demographics and claims history within your specific group. For experience rated benefits, the rates are based on the group experience (claims and your reserve), trend or inflation factors, your group’s target loss ratio, and the weight given to your claims experience.

Traditional and ASO Contracts

There are two types of funding models: traditional insurance contracts and administrative services only (ASO) contracts.

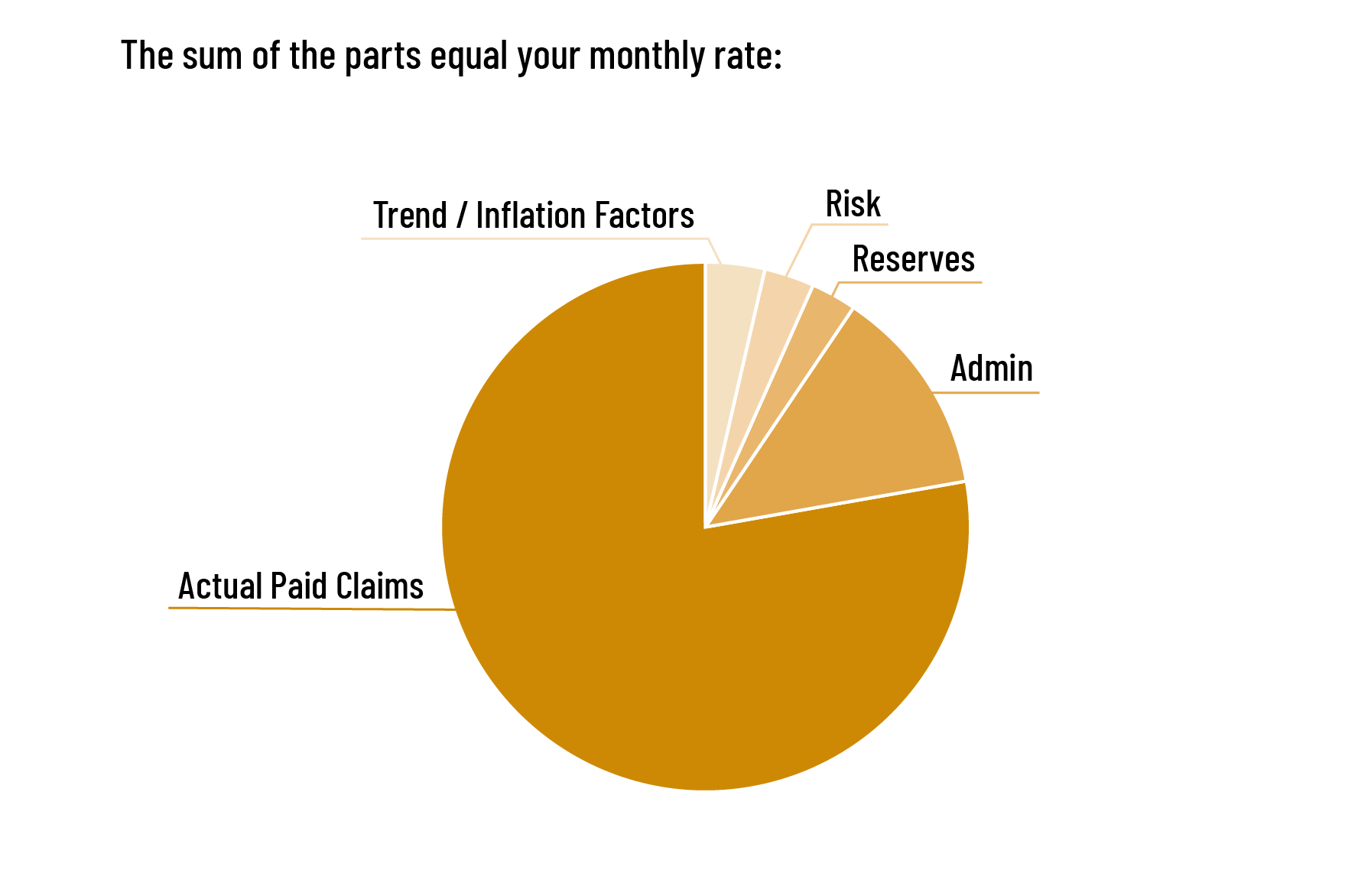

Under a traditional insurance plan, your experience rated benefits are comprised of:

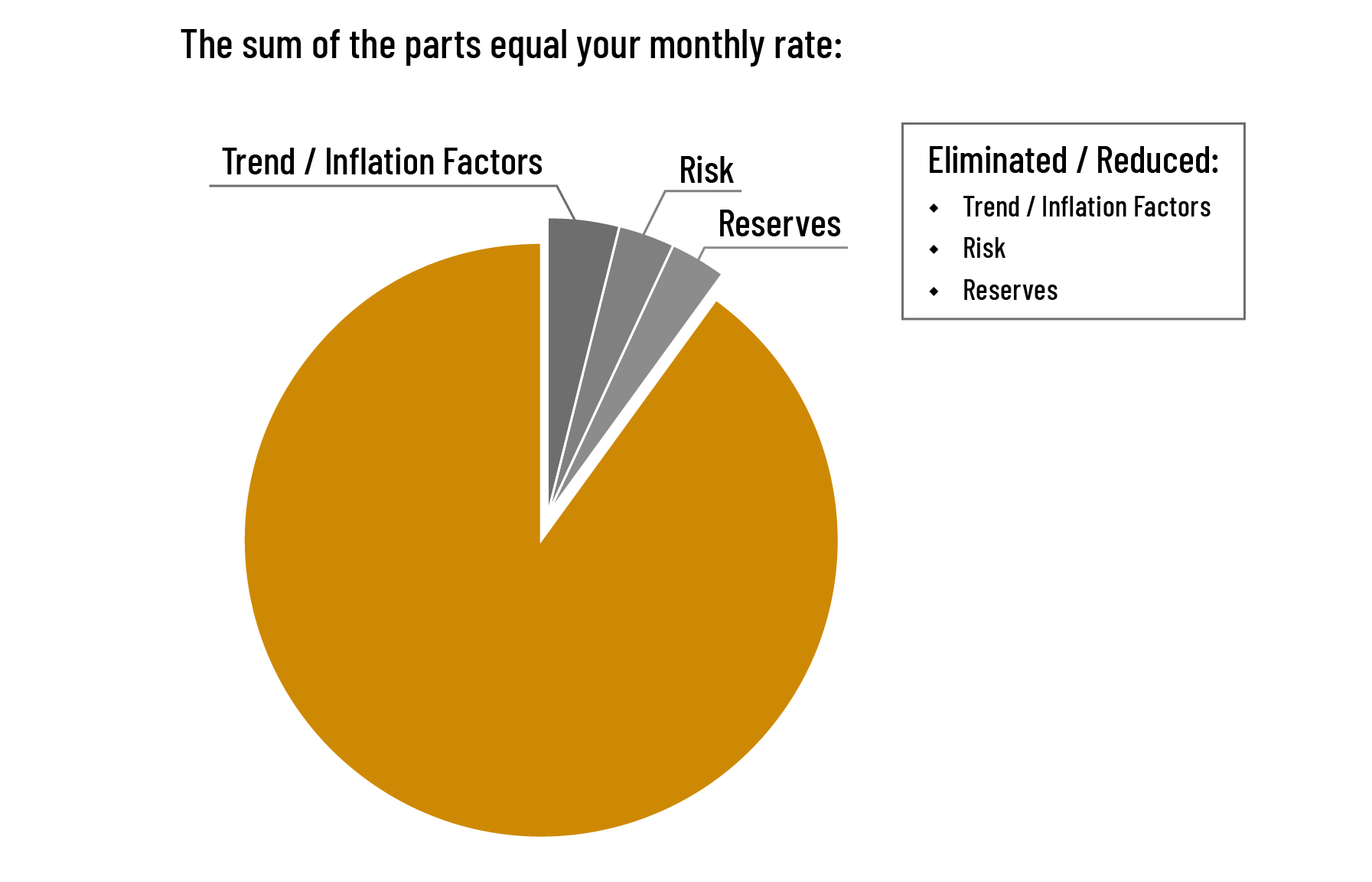

ASO contracts are an alternative kind of arrangement for your experience rated benefits, in which you agree to cover the cost of your actual claims as well as a negotiated administrative fee:

Which Model is Right For You?

| Traditional Insured | ASO | |

| If claims are less than estimates | No return of premium to employer. Typically, slight reduction in premiums upon renewal | Employer keeps the surplus |

| If claims exceed premium | No immediate exposure for employer – premiums and reserves will be adjusted upon renewal | Employer funds any deficit, but loss is capped by pooled claims included in stop loss coverage |

| Insurance for catastrophic drug claims | Yes | Yes |

| Drug card available | Yes | Yes |

| Employer / employee cost sharing of premium | Yes | Yes |

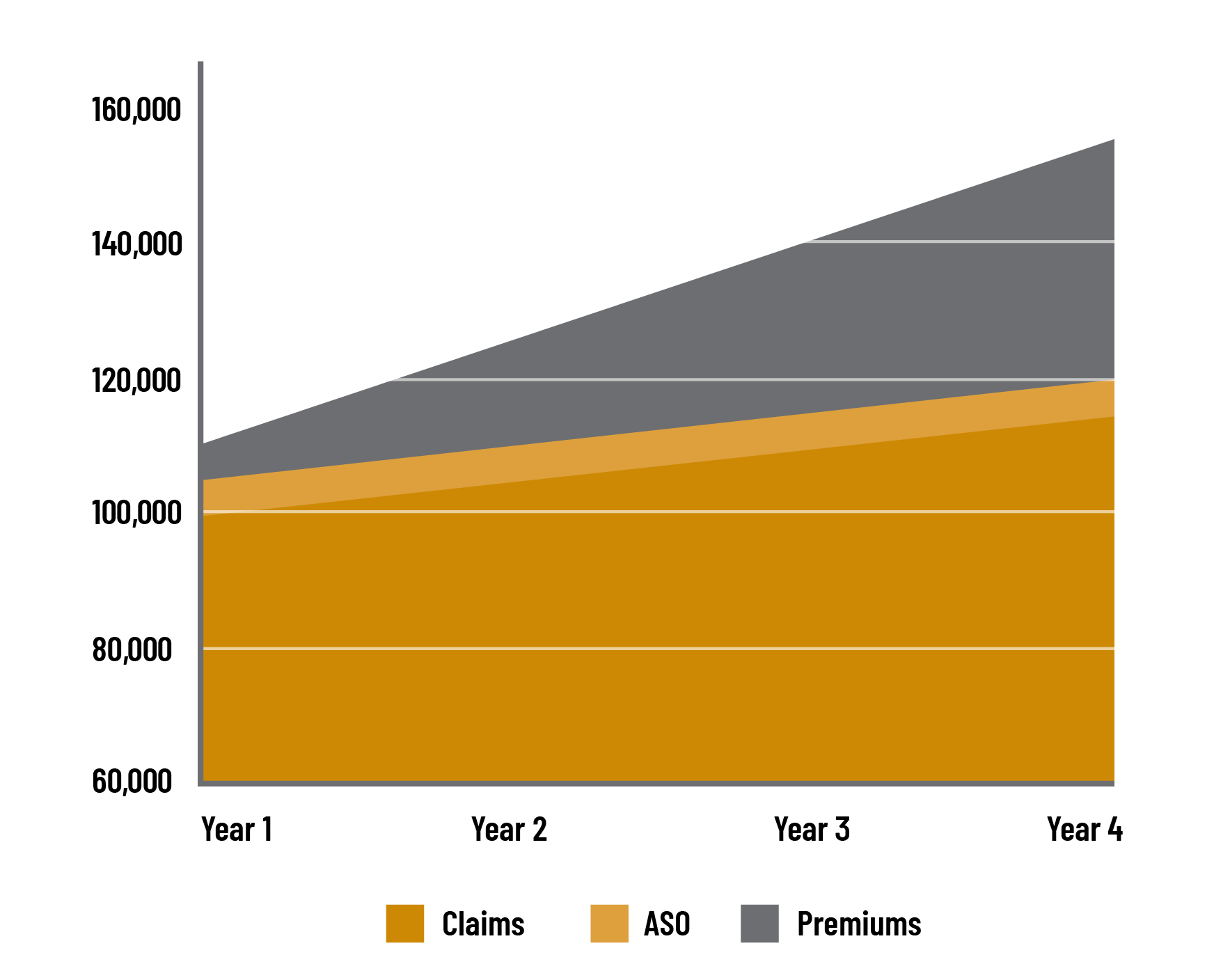

Some additional questions you may want to ask yourself are:

- Have your premiums risen at a faster rate than your claims?

- What was your total surplus between actual paid claims and premiums in the last four years?

If you see that your difference between premiums and claims is quite significant, you may wish to consider looking into an ASO funding model to prevent you from paying inflated premiums as estimated by the insurer every year.

For Your Consideration

Whether you’re on a fully insured or ASO contract, you can take advantage of the free audit offered through the RMA. The audit will provide a benchmark comparison of your current plan to industry leading models and evaluate its efficiency.

To access and get started on your free audit, click the contact button below and give us call or send us an email.